English

English  Русский

Русский Bahasa Indonesia

Bahasa Indonesia Bahasa Malay

Bahasa Malay ไทย

ไทย Español

Español Deutsch

Deutsch Български

Български Français

Français Tiếng Việt

Tiếng Việt 中文

中文 বাংলা

বাংলা हिन्दी

हिन्दी Čeština

Čeština Українська

Українська Română

Română

We remain bullish on the US dollar while the war continues. Macquarie Futures' statement echoes the centuries-old rule "buy while there's blood in the streets." The greenback, as a safe-haven asset, will indeed be in high demand during the Middle East conflict — and there's no end in sight.

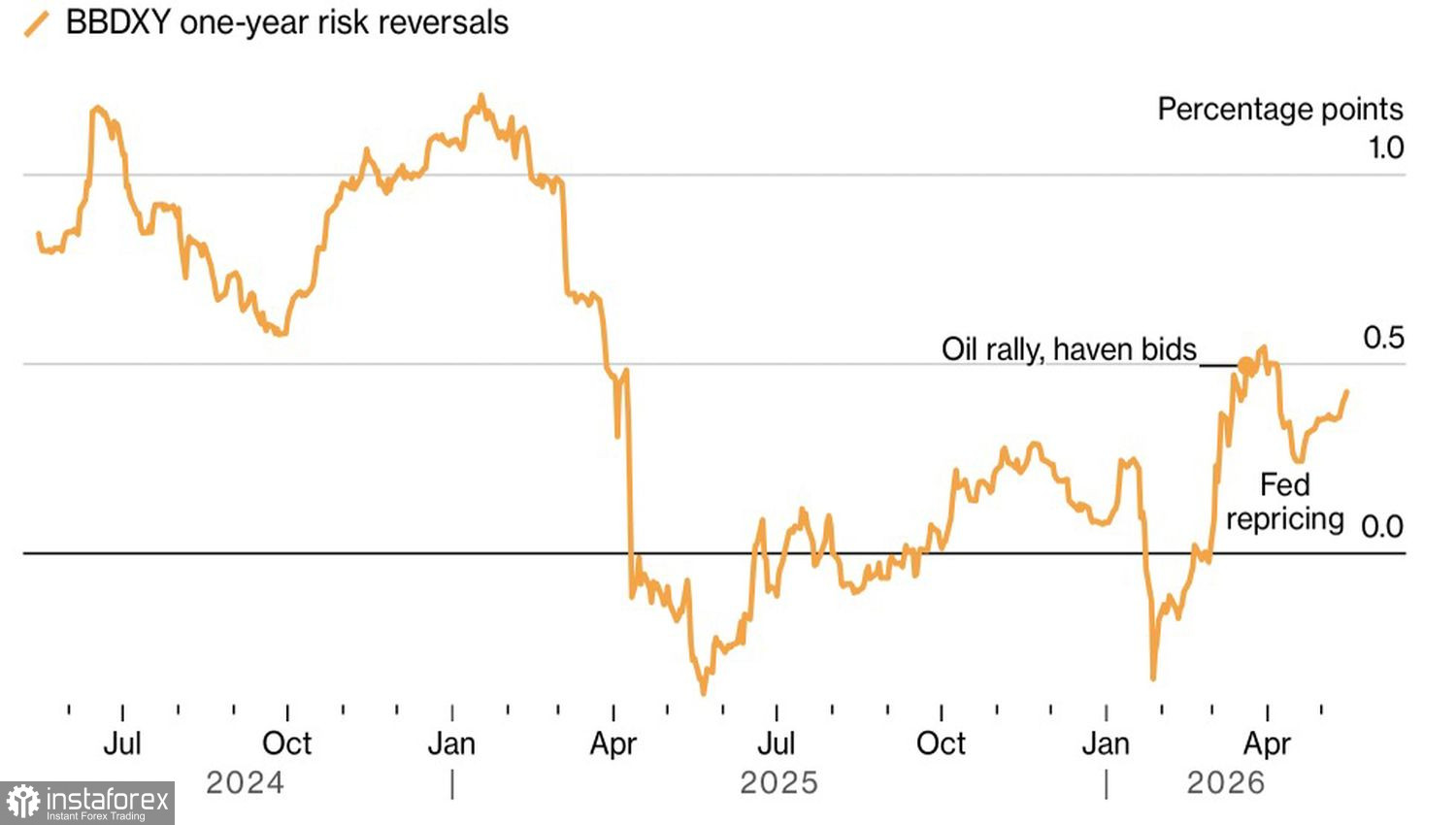

The USD index is heading for its best weekly performance in two months; reversal risks for the US dollar are skewed to the upside and are approaching the year-high seen in March. Back then, the greenback was bought both as a safe asset and as the currency of a net energy exporter. In April, bears retreated on EUR/USD on hopes that the war would end soon. It didn't. It's time to return to selling the main currency pair.

Dynamics of US dollar reversal risks

Anyone who entertained the illusion that China would pressure Iran — which sells it oil — after the Xi-Trump meeting has been disappointed. Yes, Beijing agreed that Iran building nuclear weapons would be bad, and that the blockage of the Strait of Hormuz is bad. But it does not intend to take concrete action.

The US president left China empty-handed. Worse, he was rebuked for his readiness to approve arms sales to Taiwan. China considers the island its territory and is prepared to fight for it against anyone — including the United States. Why would the White House want that? As Donald Trump put it, an armed conflict 9,500 miles away is the last thing Americans need right now.

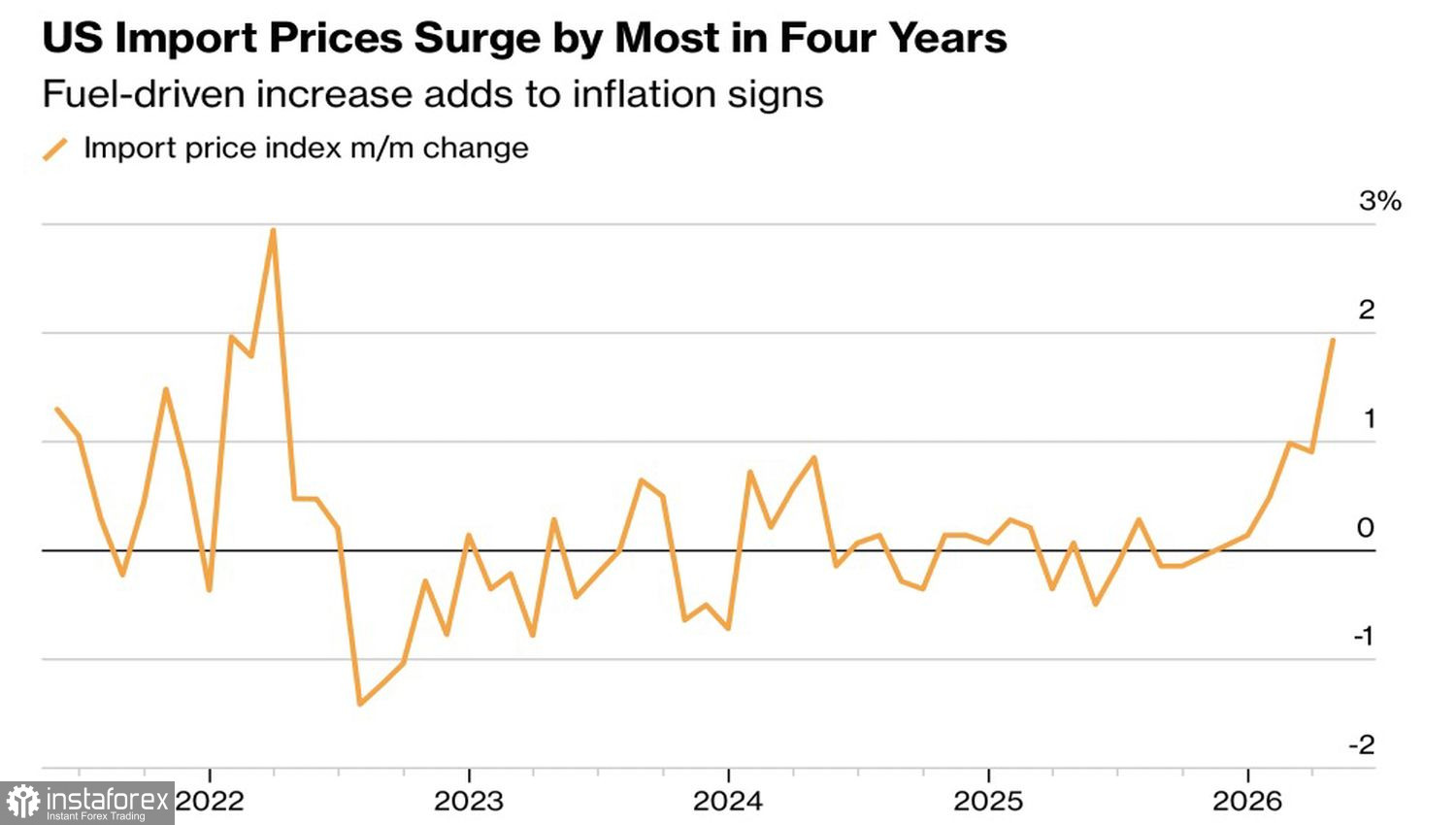

Territorial distance from the fighting in Ukraine and the Middle East, net energy exporter status and massive investments in artificial intelligence allow the US economy to thrive. The labor market has stabilized, GDP is growing at 2%, and inflation is accelerating to four-year highs. Following CPI and PPI, import prices have also risen.

US import price dynamics

If the economy is this healthy with the federal funds rate at 3.75%, it can surely withstand even higher borrowing costs. Futures markets gradually shifted the timing of Fed tightening first from April to March, and then from March to December under the influence of incoming data.

The ECB's rate-hike timetable, by contrast, is moving later. June is no longer in play amid signs of a sharp slowdown in the currency bloc's GDP. With this rate differential between the world's major central banks and the yield gap between US and German bonds, the euro has little choice but to fall.

Technically, the EUR/USD daily chart shows completion of a "Spike and Shelf" pattern. The break below the lower band of the 1.1685–1.1775 consolidation range allowed shorts opened from 1.178 to be increased. These positions should now be held and periodically added to. Target levels remain unchanged — 1.159 and 1.154.